To some spectators, many ESG funds engage in greenwashing, making little serious attempt to boost sustainability. To others, this movement is part of a woke agenda that unfairly bashes the energy industry. Yet, “not yet proven” is the conclusion of a new Luxembourg report about the effect of ESG investing on the global economy, and thus ultimately the environment and society.

Several efforts to assess the impact of sustainable finance are ongoing, but as yet no conclusions can be drawn. This was a key take-away from Tuesday’s presentation of the “Sustainable Finance in Luxembourg - A quantitative and qualitative overview” report conducted by the Luxembourg Sustainable Finance Initiative (LSFI) with PwC.

Methodologies being developed

“Some methodologies and classification schemes are gaining traction and relevance, but there is still a lack of standardisation about how to measure the impact of sustainable finance,” said Maria Eugenia Tapia Rojo, communication manager with the LSFI, a think tank backed by the Luxembourg government, Luxembourg for Finance and the High Council for Sustainable Development, a publicly funded body featuring representatives of the private and public sectors.

“Some methodologies and classification schemes are gaining traction and relevance, but there is still a lack of standardisation about how to measure the impact of sustainable finance,” said Maria Eugenia Tapia Rojo, communication manager with the LSFI, a think tank backed by the Luxembourg government, Luxembourg for Finance and the High Council for Sustainable Development, a publicly funded body featuring representatives of the private and public sectors.

The LSFI-PwC report features a review of four methodologies being developed to analyse the impact of ESG investing. The Luxembourg Institute of Science and Technology (List) is working on a project called “Refund” which estimates the life cycle sustainability of investment funds. The University of Cambridge’s Institute for Sustainability Leadership has developed the Sustainable Investment Framework which seeks to do a similar job. The IRIS+ System is a standardised approach to measure, manage, and optimise impact investing approaches being developed by the Global Impact Investing Network trade association. Meanwhile Eurosif (the European sustainable finance association) and academics from the University of Hamburg have developed a transition-focused classification for investments.

Early days

LSFI and PwC reviewed the results of this work, and found that “it is not yet possible to assess the impact of ESG fund investing impact on the economy,” said Tapia Rojo.

Yet there was a call for patience. “Institutionalised ESG is very new, yet when this matures standards will emerge which will enable more analysis to be conducted,” added Dariush Yazdani, leader of PwC’s Global AWM Market Research Centre..

Yet there was a call for patience. “Institutionalised ESG is very new, yet when this matures standards will emerge which will enable more analysis to be conducted,” added Dariush Yazdani, leader of PwC’s Global AWM Market Research Centre..

Yet even with this data, measuring the impact of this investing is fraught with difficulties. “At the moment there is no science to this, particularly in public markets,” said Frédéric Vonner, PwC's Sustainable Finance & Sustainability Leader.

“There are so many parameters that might come into play when assessing a company’s strategy. Hence it is hard to prove to what extent an ESG fund having even a low single-digit stake in a listed company might have an impact,” he said. This is somewhat different when assessing private markets, particularly if a private equity fund has a majority stake in a growth company.

“There are so many parameters that might come into play when assessing a company’s strategy. Hence it is hard to prove to what extent an ESG fund having even a low single-digit stake in a listed company might have an impact,” he said. This is somewhat different when assessing private markets, particularly if a private equity fund has a majority stake in a growth company.

Blended finance leader

However, there is substantial evidence that ESG has impacted the Luxembourg economy and financial services ecosystem. “Luxembourg is a pioneer and is very active in the field of blended finance,” said Tapia Rojo. Blended finance uses development finance to mobilise additional resources towards sustainable development in developing countries. She pointed to the EIB’s Climate Finance Platform launched in 2017, and the International Climate Finance accelerator set up here in 2018. She also highlighted the Luxembourg Green Exchange, which when it was established in 2016 listed 106 sustainable bonds and now hosts around 1,450.

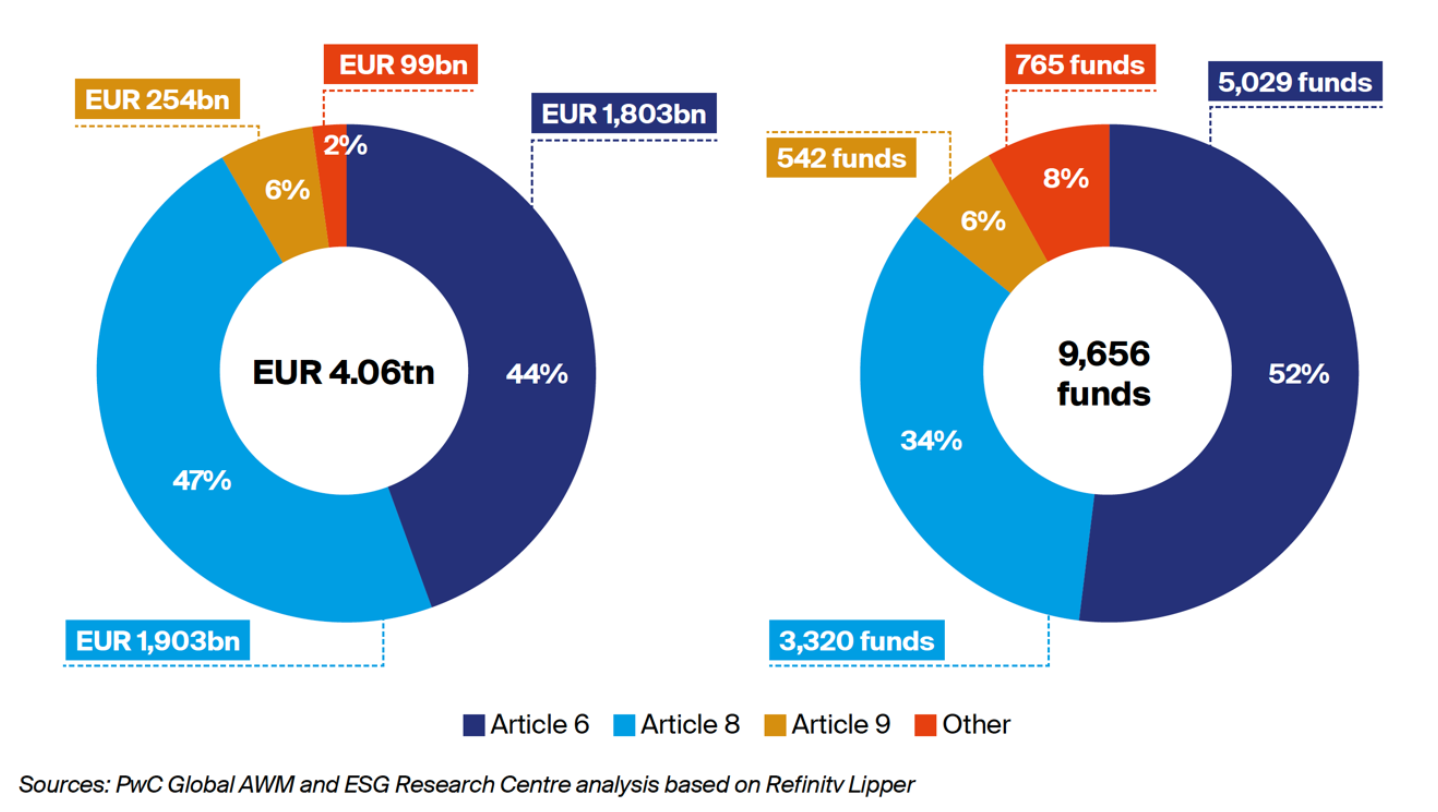

Of course, this is alongside the efforts by the Luxembourg funds ecosystem to find answers to the global asset management industry’s ESG challenges. The Sustainable Finance in Luxembourg report found that at the end of June 47 percent of assets in Luxembourg Ucits are held in article 8 funds with 6 percent in article 9 vehicles. This contrasts with one third and one in twenty of all Lux Ucits fund vehicles being classified respectively as article 8 or article 9. This is just one part of a report which analyses the ESG fund sector through different angles.

SFDR reclassification evidence

Asked to what extent he is seeing a generalised reclassification process within these SFDR categories, Vonner pointed to data indicating that a few dozen funds had moved from nine to eight or eight to six in the third quarter. As for the future: “let's wait and see the figures for Q4. With the entrance into force of the SFDR level 2 measures from January 1, asset managers have been working to refine the marketing documentation, pre contractual information and so on. This might lead to a further increase in reassessment,” he said.

SFDR split by AuM and number of funds

as of June 2022 for Luxembourg