Housing markets in major cities across the world face a “prolonged stagnation” in purchase prices and a price correction. House owners and real estate investors should not expect the market to trend sideways. It's “game over” for housing markets, Swiss bank UBS writes in its latest Real Estate Bubble Report.

With a rise in interest rates, finance costs have increased while financial markets across the world have been rocked by geopolitical developments and severe declines in asset prices.

“Consequently, the willingness to pay for owner-occupied homes is likely to take a hit,” the UBS report said. “In cities with strong population growth, such an adjustment could manifest in the form of a prolonged stagnation in nominal purchase prices and a price correction in real terms—i.e., adjusted for inflation. But as real estate markets rarely trend sideways, this is not the most likely outcome.”

Labour market as last pillar

In a paragraph headlined “Game over”, the UBS report noted that a “robust labour market” remains the last pillar of support for the owner-occupied housing market in most cities. “With a deterioration of economic conditions, this too is at risk of faltering. Indeed, we are witnessing the global owner-occupied housing boom finally under pressure, and in a majority of the highly-valued cities, significant price corrections are to be expected in the coming quarters.”

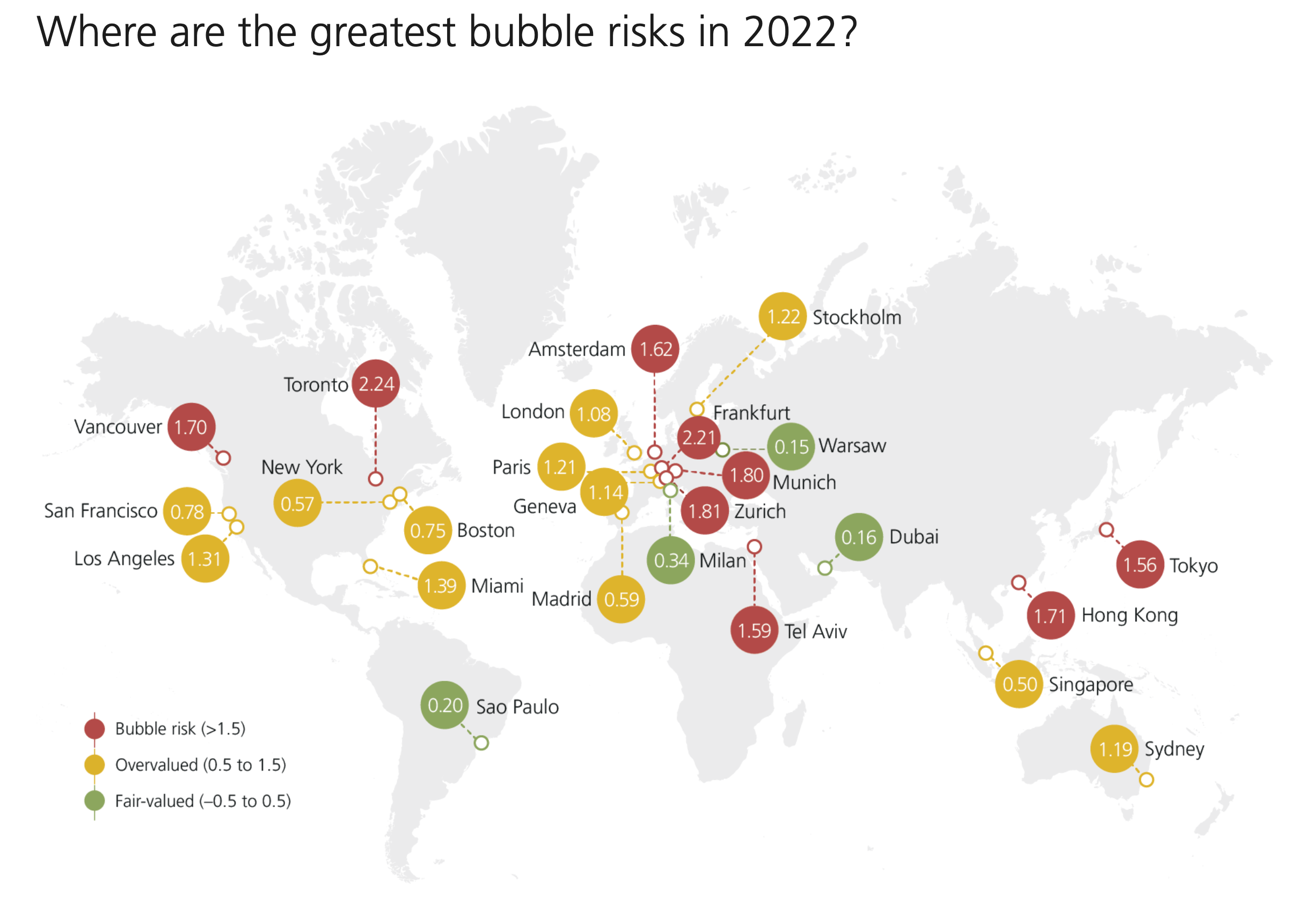

Looking at Europe, UBS’s report pointed to bubble-like conditions in five major cities, including Frankfurt, Zurich, Munich and Amsterdam. The bubble index for these cities ranged between 2.21 for Frankfurt and 1.61 for Amsterdam.

Bubbles are a recurring phenomenon in property markets, UBS explained. The term “bubble” refers to a substantial and sustained mispricing of an asset, the existence of which cannot be proved unless it bursts. But historical data reveals patterns of property market excesses.

The UBS Global Real Estate Bubble Index gauges the risk of a property bubble on the basis of such patterns. The index does not predict whether and when a correction will set in. A change in macroeconomic momentum, a shift in investor sentiment or a major supply increase could trigger a decline in house prices.

One room less in Munich

Toronto topped the list, together with Frankfurt, with both of these markets exhibiting pronounced bubble characteristics, said UBS. Frankfurt, like Munich, risks a drag on demand due to a subdued economic outlook and higher mortgage rates. “A skilled worker from the service sector can now buy an apartment with one room less in Munich on average than before the pandemic,” it said.

The Luxembourg housing market is not addressed in the UBS report. Last March, the International Monetary Fund expressed its concerns over house prices in the grand duchy.

IMF worries for Luxembourg

Actions were urgently needed to reduce pressures in the housing market, the IMF said at the time. “In addition to posing medium-term financial stability risks, the rapid pace of housing price growth is affecting affordability, and, if continued, could reduce Luxembourg’s attractiveness for workers.”

“To mitigate imbalances in the housing market, efforts to increase supply should be accelerated,” the IMF said. “Rapidly growing housing prices, for the third consecutive year, raise concerns about affordability, attractiveness for workers, and medium-term financial stability.”

According to Luxembourg's real estate website Immotop, the average price in the country reached its peak in July with an average value of 9.208 euro per square meter. That compares to 7.710 euro per square meter in November 2020. Prices in Luxembourg city are seen spiking at between 15.000 and 20.000 euro per square meter, with new studio apartments of 35 square meters being offered for 600.000 euro or more.

The Amsterdam housing market saw the strongest price growth among Eurozone cities analysed at 17 percent between mid-2021 and mid-2022 in nominal terms, after nominal property prices doubled within the last ten years.