Can high yield be a substitute for equities in this low growth environment?

As investors, we are often liable for thinking in specific asset class buckets rather than taking a broader view of the investment universe. Yet, taking a cross-asset class view could assist in smarter investment choices and allocations. This perspective is very visible when comparing high yield bonds to equities: two investments that sit in very different asset class buckets, however, their risk-return characteristics are more similar than most imagine and could be viewed as competing asset classes. So much so, that we would argue that high-yield bonds could be considered as an alternative to equities, but with lower volatility.

For investors this consideration could be relevant when looking ahead to 2023. For example, the Global High Yield market is currently offering investors a yield of around 9%[1] which represents levels that, historically, have been associated with subsequent positive returns. Alongside this, high yield markets are of better credit quality in general than in the past which means that although defaults are likely to rise in this challenging environment, they are expected to stay contained. On the other hand, it is likely that factors such as a deteriorating earnings outlook and continuing high interest rates will remain headwinds for equities for some time. Against this backdrop, for investors looking for equity-like returns, high yield may provide them with such a solution.

High yield vs Equities: volatility is a differentiator

Overall, there is a high correlation between high yield and equities: global high yield and global equities have had a correlation of 0.83[2] over the last 10 years. Even at a regional level, the correlation between these two asset classes is high: US is 0.79 and Europe 0.75[3]. This demonstrates how investors may start to think of high yield as an alternative to equities because the two should perform in relatively similar manners.

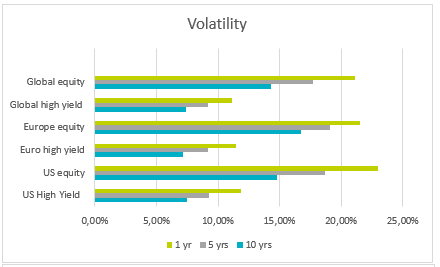

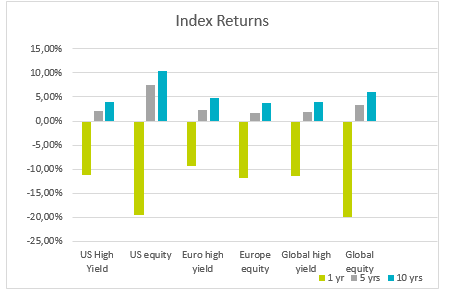

This correlation is reflected, on the whole, in returns. Over a 10 year time period, global high yield has largely kept pace with global equities: 3.98% and 5.95% respectively[4]. While, the returns for global equities have outperformed global high yield in stronger years, in 2022 with markets falling, global high yield provided investors with a relatively better return than equities: -11.39% for global high yield versus -19.8% for global equities over the year[5]. To that measure, high yield bonds behaved as you would expect a bond to behave against equities - providing some protection during periods of negative markets while also not gaining as much when markets are strong. But it is the difference in volatility levels that is a key differentiator between high yield and equities and one that could be relevant coming into 2023 as many of the risks from the last 12 months persist. As the charts below demonstrate, high yield across the three main investment universes offers a lower volatility than equities with, often, similar returns.

Volatility and Index Return Comparison [6]

How they differ in structure:

Of course, volatility is not the only differentiator. In order to generate returns on equities, you need earnings growth or multiple expansion. However, as an investor in high yield, your return is more reliable as it comes from your coupon payment. High yield debt also benefits from interest rate exposure which can help to mitigate losses during periods of volatility.

As well as this, debt sits above equity in a company’s capital structure, meaning that in the event it is listed, a company will halt dividend payments to shareholders before coupon payments to bondholders are interrupted.

It is difficult to discuss debt without referencing default risk when it comes to high yield. While we expect the default and downgrade rates to increase this year in reaction to economic challenges, we believe they will remain relatively low compared to other periods of turbulence. We believe that the key to successful high yield investing is in avoiding those companies likely to be subject to a deterioration in credit quality and therefore to avoid capital loss.

As we begin 2023

We expect many of the same risks from 2022 such as inflation and geopolitical challenges that are likely to continue to worry investment returns in 2023. The benefits of a diversified portfolio are not difficult to appreciate in such times, but how investors allocate within that and analyse their allocations is more nuanced. Indeed, generating equity returns from multiple expansion and earnings growth may be more difficult to achieve in a low growth environment, while compounding income from high yield debt could offer more reliable returns. With equity-like returns but lower volatility, it may be worth considering high-yield bonds as an alternative to equities especially in these unpredictable markets.

Glossary

Default Risk: The risk of an issuer not being able to repay their debt obligations.

High Yield Debt: Also known as “junk” bonds, are issued by companies with a lower credit rating than their investment grade counterparts.

Volatility: the degree of variation of a price for a given security or market index. As a rule of thumb, the higher the volatility, the riskier the security.

[1] Source: AXA IM, Bloomberg as at 11 January 2023

[2] Source: AXA IM, Bloomberg as at 31 December 2022. Based on ICE BofA Global High Yield Index and MSCI All Country World Index

[3] Source: AXA IM, Bloomberg as at 31 December 2022. Based on ICE BofA US High Yield Index, ICE BofA Euro High Yield Index, S&P 500 Index and Eurostoxx 50 Index

[4] Source: AXA IM, Bloomberg as at 31 December 2022. Based on ICE BofA Global High Yield Index and MSCI All Country World Index

[5] Source: AXA IM, Bloomberg as at 31 December 2022. Based on ICE BofA Global High Yield Index and MSCI All Country World Index

[6] Source: AXA IM, Bloomberg as at 31 December 2022. Indices are: US high yield: ICE BofA US High Yield Index; US equities: S&P 500 Index Euro High Yield: ICE BofA Euro High Yield Index; Europe Equities: Eurostoxx 50 Index; Global High Yield, ICE BofA Global High Yield Index and Global Equities: MSCI All Country World Index

Not for Retail distribution: This promotional communication is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by the MiFID (2014/65/EU). Circulation must be restricted accordingly.

This communication does not constitute on the part of AXA Investment Managers or its affiliates a solicitation or investment, legal or tax advice. This material does not contain sufficient information to support an investment decision.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this communication is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this communication. All exhibits included in this communication, unless stated otherwise, are as of the publication date of this communication.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Before making an investment, investors should read the relevant Prospectus and the KIID, which provide full product details including investment charges and risks. The information contained herein is not a substitute for those communications or for professional external advice. These documents are available free of charge from AXA IM Benelux, Place du Trône 1 - 1000 Brussels, and via the website www.axa-im.be in French and Dutch.

For European Investors:

Please note that the management company reserves the right, at any time, to no longer market the product(s) mentioned in this communication in a European Union country by notification to its authority of supervision in accordance with European passport rules.

In the event of dissatisfaction with the products or services, you have the right to make a complaint either with the marketer or directly with the management company (more information on our complaints policy https://private-investors.axa-im.be/fr/plainte). You also have the right to take legal or extra-judicial action at any time if you reside in one of the countries of the European Union. The European online dispute resolution platform allows you to enter a complaint form (https://ec.europa.eu/consumers/odr/main/?event=main.home2.show) and informs you, depending on your jurisdiction, about your means of redress (https://ec.europa.eu/consumers/odr/main/?event=main.adr.show2).

A summary the investors' rights is available in French and Dutch on our website https://private-investors.axa-im.be/fr/resume-des-informations-concernant-les-droits-des-investisseurs

Any reproduction, in whole or in part, of this communication is strictly forbidden without the express prior consent of AXA IM. AXA Investment Managers Paris shall not be held liable for any decision taken on the basis of this information.

Issued by AXA Investment Managers Paris, a company incorporated under the laws of France, having its registered office located at Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 353 534 506, and a Portfolio Management Company, holder of AMF approval no. GP 92-08, issued on 7 April 1992.

Distributed in Belgium and Luxembourg by AXA IM Benelux, a company incorporated under Belgian law with its registered office at Place du Trône, 1, B-1000 Brussels, registered in the Brussels Trade Register under number 604.173.

Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.

© AXA Investment Managers 2023. All rights reserved.