Why our focus on value and active stock-picking should provide a winning combination for investors.

There now seems little doubt that the market rotation away from technology-heavy growth stocks towards more cyclical value stocks is well underway. The return of the MSCI All Country Value Index (+13.2%) is almost double that of the growth equivalent (+7.6%) so far this year[1], adding momentum to the shift that began in early November when the breakthrough of COVID vaccinations was first announced.

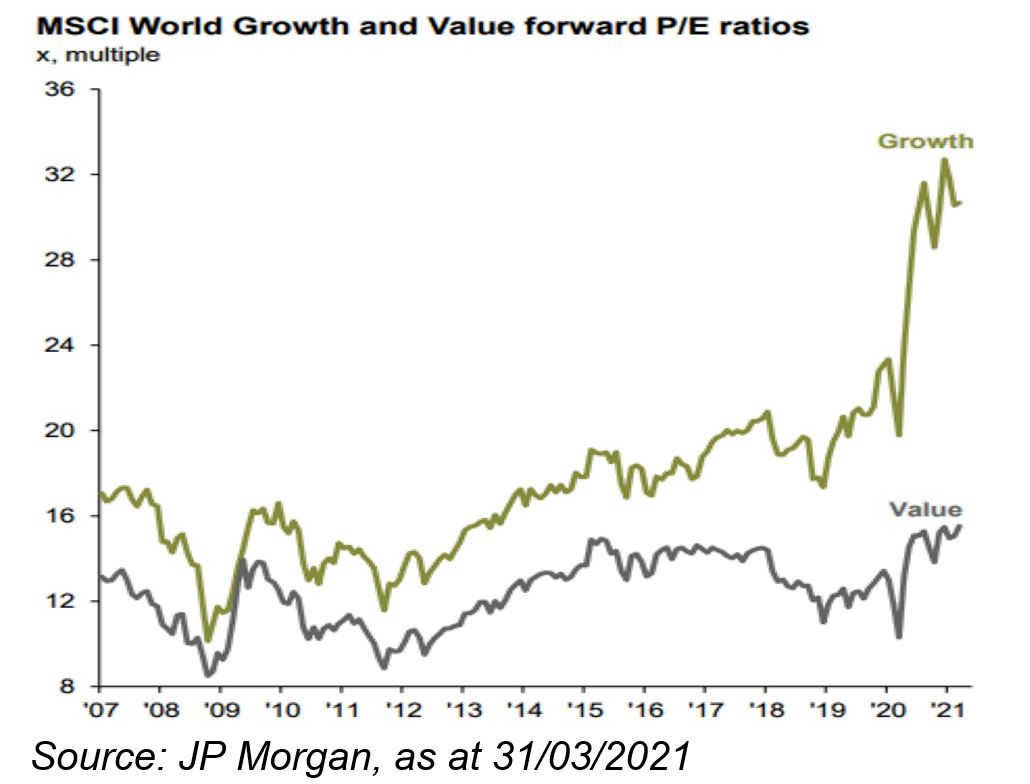

Despite this strong reversal, the valuation spread between growth and value stocks remains huge on most measures. The two most common, which compare a company's share price to expected future earnings (forward Price/Earnings) or the value of its assets (Price/Book) show that value stocks globally currently trade at discounts of 50% (see chart) and 70%, respectively[2]. This highlights the catching-up that value still has to do following a decade of underperformance – these discounts have averaged 32% and 50% over the last 20 years[3] – but also that the best days for value investors like SKAGEN are likely still to come.

Earnings boost

As countries around the world begin to emerge from lockdowns, value stocks such as financial, industrial and energy companies should outperform as they tend to experience growing demand and profitability in post-recessionary phases of the economic cycle. These environments are also supportive for cyclical sectors like restaurants, hotels, airlines, high-end retailers and car manufacturers which sell discretionary goods and services that are in demand when the economy is growing and consumer confidence is high.

Companies from these sectors – which conversely suffered most during the pandemic – are well represented in our portfolios, while the anticipated recovery in real estate as offices reopen alongside retail, hospitality and entertainment premises should boost SKAGEN m2.

In many countries the recovery is being turbo-charged by government stimulus, particularly the US where President Biden has injected trillions of dollars into the economy. This is creating inflationary pressure that has seen long-term interest rates almost double since the turn of the year[4]. The next phase of the value rotation could be driven by Europe where the vaccine roll-out has so far been slower and long-term interest rates remain negative, holding back the performance of financial and economically-sensitive stocks relative to the US.

Emerging markets could also provide value with further impetus during the second half of the year as India and Brazil hopefully start to win difficult battles against COVID and their economies emerge from lockdown. Finally, the influence of momentum-focused traders and quant-driven funds cannot be over-looked. They played a big role in pushing growth stocks ever higher in recent years and could propel value companies upwards if they continue to gain traction.

Picking winners

A feature of the pandemic has been the decoupling of share prices from economic reality. Equity markets – largely supported by technology and 'quality' stocks – have continued to rise despite GDP falling off a cliff. As we approach the end of the tunnel, economic recovery is increasingly being priced in for stocks in other sectors and the key challenge for investors is to find those offering the most value.

It is in this environment of economic growth and a fragmented stock market that active management should come in to its own. Investing in a passive fund that tracks an index – even one with a 'value' label – is fraught with risk. Most value indices are constructed using basic valuation screens that favour stocks with low Price/Book and Price/Earnings multiples or high dividend yields, which ignore important company characteristics and risk factors.

At SKAGEN we also use these tools as part of our investment process, but each has well-documented limitations and relying on them can lead to investing in companies that are optically cheap but represent value traps. To navigate these, we have an extensive library of thoroughly researched companies – analysed using both quantitative and qualitative techniques – that help us to pick the right stocks at the right time.

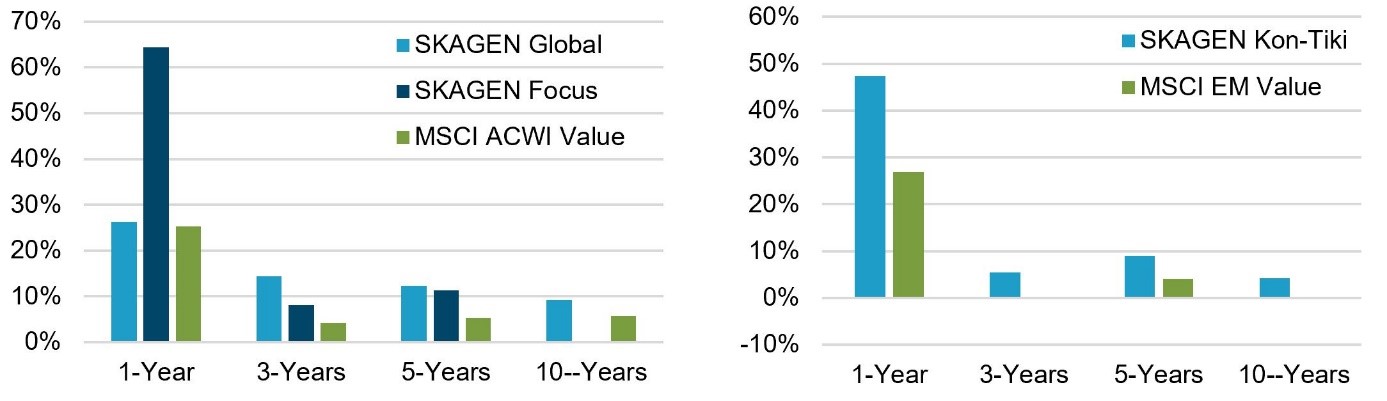

These benefits are illustrated by the performance of our funds against comparable MSCI value indices that are available. SKAGEN Global and SKAGEN Focus, which both use the MSCI All Country World Index as their formal benchmark, have beaten the value sub-index over 1, 3, 5 and 10 years while SKAGEN Kon-Tiki, which is formally benchmarked against the MSCI Emerging Market Index, is ahead of the value version over the same time periods[5]:

Our funds have consistently delivered strong returns both in absolute terms and relative to comparable value indices

There are key features of SKAGEN's approach to active investing that enable our funds to deliver these strong returns. First, broad mandates mean that we have the freedom to invest wherever we see the best opportunities at a particular time. They also allow us to invest with conviction in our best ideas. A recent study[6] added further weight to previous research showing that the best performing active managers hold the most concentrated portfolios over time. Finally, we invest long-term and while we anticipate that many of our portfolio holdings will benefit from economic recovery, we place greater weight on the earnings power of companies over a multi-year investment horizon to generate the best long-term returns for our clients.

On the back of six months' outperformance, value is still at an attractive discount to growth and with the strong winds of economic recovery in its sails, value investing could well be a generational opportunity. With all SKAGEN's equity funds delivering strong absolute returns this year and with four of five ahead on a relative basis, our active approach should put clients in the sweet spot for the best possible risk-adjusted rewards.

For more articles on SKAGEN Funds and our range of value funds, please visit www.skagenfunds.com or contact me at

e-mail: michel.ommeganck@skagenfunds.com

Mobile phone: +4790598412

[1] Source: MSCI. 31/12/2020 – 30/04/21 in EUR [2] Source: MSCI: MSCI ACWI Value Index vs. MSCI ACWI Growth Index as at 31/03/2021 [3] Source: Bloomberg. Average forward P/E and P/B for MSCI ACWI Value and MSCI ACWI Growth 2001 – 2021 [4] US 10-year Treasury Yield 31/12/20 – 05/05/21 [5] In EUR as at 30/04/2021 and annualised for periods over 1 year. SKAGEN fund performance net of fees. Source for MSCI indices: MSCI. [6] Source: The journal of Portfolio Management, The Decision to Concentrate: Active Management, Manager Skill, and Portfolio Size, 2020