Investors are bracing for an inflection point in Federal Reserve policy, from adding monetary stimulus to gradually paring it back. This is not the 2013 taper tantrum, but a telegraphed taper, according to Evan Brown, head of multi-asset investment at UBS Asset Management.

In his latest Macro Monthly, Brown writes that investors are underappreciating the likely strength of economic growth which is unlikely to be derailed by central banks tip-toeing away from the extraordinary easing policies.

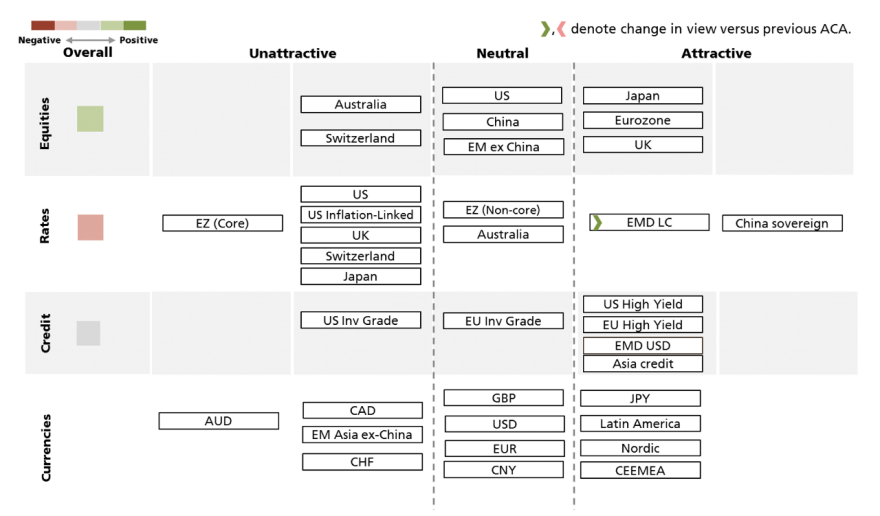

Highlights from the Macro Monthly are:

- For equities, continued earnings growth is likely to outweigh any negative effects of a Fed taper.

- We believe that investors are underestimating the strength of the expansion, which is providing opportunities in procyclical positions.

- There are welcome signs of a shift to a healthier nominal growth environment ahead, with more real activity and ebbing inflationary pressures.

- In our view, a still slow-moving Fed and cyclical acceleration favors higher long-term bond yields and outperformance for pro-cyclical sectors and regions.

A withdrawal of central bank stimulus is a natural, welcome consequence of a global economic recovery that continues apace – even as the Delta variant prevents a full normalization of activity. However, the low level of longer-term bond yields and equity market internals currently imply that that the economy is ill-equipped to handle even modest adjustments to this highly accommodative policy setting.

We believe this view is misguided. On its own, the nascent withdrawal of US monetary stimulus is not a threat to the economic expansion, as activity is likely to stay well above trend in 2022. As such, it is not a threat to the earnings growth that underpins the equity bull market.

Here you'll find the complete Macro-Monthly 'Telegraphed taper no threat to the expansion' from UBS Asset Management.