In 2020, economic damage was driven by the need to flatten the infection curve. The evolving expansion in 2021 is tied to the steepening curve of vaccinations.

UBS Asset Management enjoyed success in their procyclical positioning in the second half of 2020, as the asset manager expected investors to be able to look through near-term difficulties to the broadening, durable recovery around the corner.

This view will inevitably be tested in 2021 by the challenges of vaccine administration, the potential for ebbing global fiscal and monetary stimulus, and other hitherto unforeseen obstacles, UBS AM's experts say in their new Macro Quarterly.

Market volatility

UBS AM is prepared for market volatility should the identifiable risks on the horizon be realized, which could cause detours along the path to normalization but not an economic downturn.

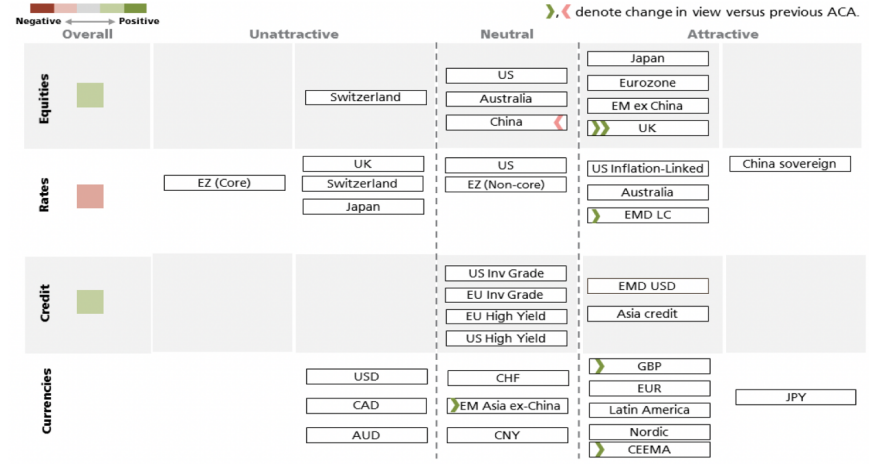

This direction of travel is positive, and UBS AM believes it provides an attractive backdrop for risk assets. The trade set that historically has performed well in an early-cycle environment includes US dollar weakness, value over growth, small caps vs. large, non-US risk assets over their US counterparts, cyclical stocks vs. defensives, and a steepening yield curve. UBS AM believes that these typical beneficiaries have substantial room to run on the nonlinear but eventual progress towards pre-pandemic norms.

UBS AM believes 2021 will bring about the realization, and in some cases, continuation of many trends the investment experts anticipated would unfold in early 2020 before the pandemic derailed all macro prognostications. And for the same reasons, to boot: An expected cyclical upturn leaves us constructive on global equities, and should disproportionately benefit non-US stocks and weigh on the US dollar.

Changes in the fundamental backdrop over the past year have made these relative value opportunities even more compelling and resilient to shocks.

The degree of policy support provided in 2020 increases the conviction in superior earnings growth and outperformance of more cyclically oriented sectors and country indexes going forward. And because of the past price performance, the valuation discrepancies are even wider, creating a more attractive opportunity with a higher margin of safety.

Procyclical forces

The observed interest rate convergence, reinforced by a structural dovish policy shift from the Federal Reserve, should leave the US dollar out of favor, especially compared to high-beta emerging market currencies.

UBS AM’s experts believe that Europe’s more collectivist approach to fiscal policy will begin to bear fruit in 2021, and EU restrictions that limit national borrowing will stay suspended. China has also pledged that while credit growth will slow, there will be no abrupt departure from its macroeconomic stabilization initiatives.

The Federal Reserve (Fed) has indicated that it will not overreact to any short-term burst of inflation in 2021, and will wait for more persistent signs of price pressures before considering the withdrawal of stimulus. Other developed-market central banks are also poised to maintain highly accommodative policy in order to help foster the strongest and most widely-shared recovery possible. In doing so, they will be buoying procyclical forces in 2021 simply by standing still as the expansion gains traction, inflation picks up, and realized real rates decline.

UBS AM believes sticking with a procyclical playbook through most obstacles that may emerge in 2021 is the best approach, as vaccination efforts allow economic momentum to be reclaimed.

Here you'll find the complete Macro Quarterly from UBS Asset Management.