Luxembourg's financial watchdog, the Commission de Surveillance du Secteur Financier (CSSF), has set a deadline of Dec. 31, 2023, for investment funds and their managers to conduct comprehensive assessments of their valuation frameworks and to update these where necessary.

The review, like the CSSF’s contentious fund cost review announced last year, stems from a common supervisory assessment, or CSA, by the European Securities and Markets Authority, Esma. The CSSF's directive has been set out in a 19-page report released on 18 July. Esma issued its guidance on 24 May when it posted its CSA report and reported on shortcomings, weaknesses and vulnerabilities in the valuation of European funds.

“Through these reports, CSSF and Esma are further elaborating regarding their expectations of valuation frameworks,” said Rafaël le Saux, who leads a team of valuation specialists at PwC Luxembourg. “One of the key takeaways is the request for more detailed and comprehensive valuation policies and procedures, clearly allocating tasks and responsibilities.”

“Through these reports, CSSF and Esma are further elaborating regarding their expectations of valuation frameworks,” said Rafaël le Saux, who leads a team of valuation specialists at PwC Luxembourg. “One of the key takeaways is the request for more detailed and comprehensive valuation policies and procedures, clearly allocating tasks and responsibilities.”

Wave of support requests expected

Fund valuation professionals, especially those working for third-party consultancy firms, now brace themselves for a wave of support requests from Luxembourg management companies once the holiday season is over. In many cases, one expert explained, fund valuation policies are too broad, reporting is not frequent enough while reports generally lack in detail.

Valuation procedures for thousands of alternative investment funds in particular will have to be reviewed, according to people familiar with the requirements. Such funds in recent years have experienced strong growth and now account for about a third of the 5,000 billion euro in funds domiciled in the Grand Duchy.

The CSSF order to evaluate their valuation frameworks applies to all investment fund managers managing regular Ucits funds and/or alternative investment funds (AIFs). If necessary, they must take corrective measures by the year-end deadline, CSSF said.

Some AIFMs may be challenged

One regulatory expert familiar with valuation practices in Luxembourg said the review may be particularly challenging for smaller firms licensed as Alternative Investment Fund Managers, or AIFMs. Luxembourg was home to 259 AIFMs at the end of 2022, including a wide ranging mix between established major Management Companies and a range of smaller firms that attracted fund business through highly competitive rates in recent years.

As part of Esma’s supervisory action, CSSF last year already asked 30 investment fund managers to report valuation practices for a total of 412 umbrella Ucits funds and open-ended alternative funds, including 38 foreign funds. The CSSF findings have been reported to Esma but have not been made public.

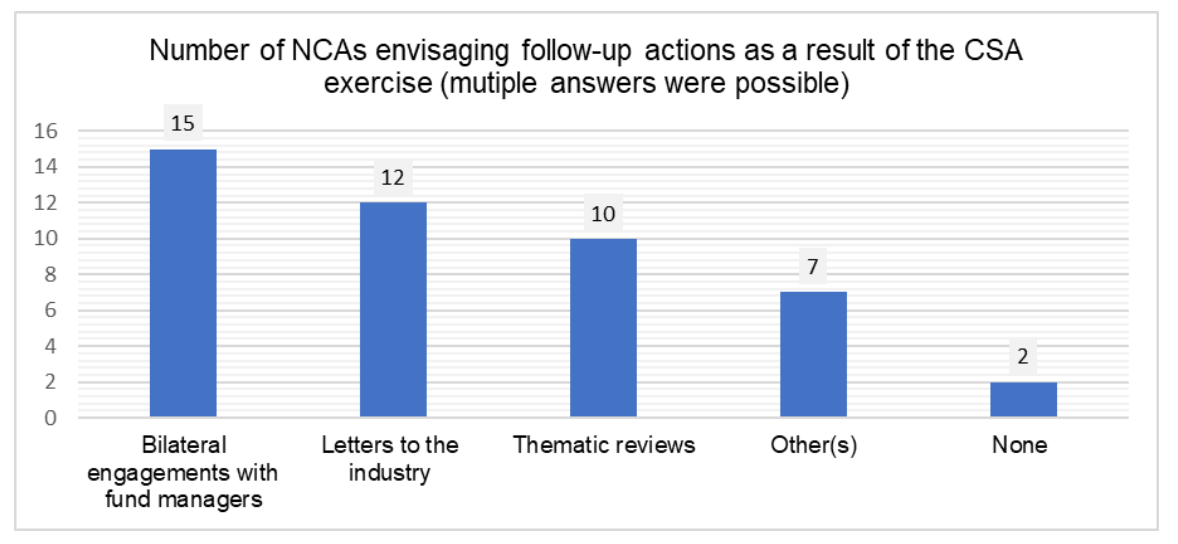

Esma, in its CSA report, did not comment on specific findings, declining to name national supervisors nor country names. It did disclose however that nine national supervisors had found breaches of regulation. Two unidentified supervisors had decided to initiate enforcement actions in a total of seven cases.

‘Room for improvement’

Generally speaking, Esma found “a satisfactory level of compliance” with “room for improvement on a few deficiencies” which were detected: a lack of documented and established valuation policies and a lack of a clear definition of the valuation model to be applied, as well as its validation. Furthermore, it noted a lack of systematic liquidity stress testing.

Esma also said issues arose in some specific cases with regards to the lack of independence of the valuation function, and smaller managers which, in some instances, appeared to over-rely on third-party data providers for the pricing of less liquid assets, without performing the appropriate checks, controls and back testing.

Issues also arose in the alignment between the NAV calculation, the asset valuation frequency and the availability of up-to-date data for private equity funds and funds invested in less liquid assets and, even more so, for those funds offering daily redemptions, such as some types of Real Estate funds, Esma said. Such funds are highly prevalent in Luxembourg, which considered itself a hub for private equity and real estate funds.

Ucits model does not work for AIFs

Le Saux, who also serves as vice chairman of the Luxembourg Valuation Professionals Association, pointed out that certain industry participants find the legal requirements that govern fund valuations in Luxembourg challenging to interpret and, therefore, welcome the additional guidance from the CSSF feedback report.

Luxembourg is home to some 14,000 alternative investment funds that all have their own different characteristics, ranging from venture capital and private equity to private debt, infrastructure and real estate markets. The applicable rules are heavily modelled on the Ucits funds, which account for the bulk of assets domiciled in Luxembourg.

CSSF, in its July communication, said it currently is actively engaging with the fund managers in its 2022 sample, requiring them to rectify the identified weaknesses, shortcomings, and vulnerabilities. The Esma findings also have given reason to launch the comprehensive valuation assessment for the entire fund sector.

Fund valuation review triggers follow-up across Europe