European pension savers are facing significant hurdles due to high fee levels and a lack of transparency in pension savings markets.

A European pensions watchdog's new report also highlights difficulties in accessing essential data on costs and performance, and calls on national authorities to push for more transparent and coherent reporting frameworks and standardised reporting requirements.

The Better Finance Pensions Report 2023 highlights the urgent need for comprehensive measures to secure the financial futures of millions of European pension savers, detailing the challenges they face and offering extensive policy recommendations. Better Finance is a Brussels-based NGO standing up for the rights of users of financial services.

Its report reveals critical issues in Europe's pension savings markets, including high fees and lack of transparency, challenging savers to make informed decisions.

Urgent reforms needed

The Better Finance report urges immediate action from both EU and national authorities, focusing on implementing rules for product oversight, governance, and investor information dissemination. It stresses the importance of harmonised reporting standards, reducing conflicts of interest in scheme management, enhancing governance, and providing clear, comparable information to investors.

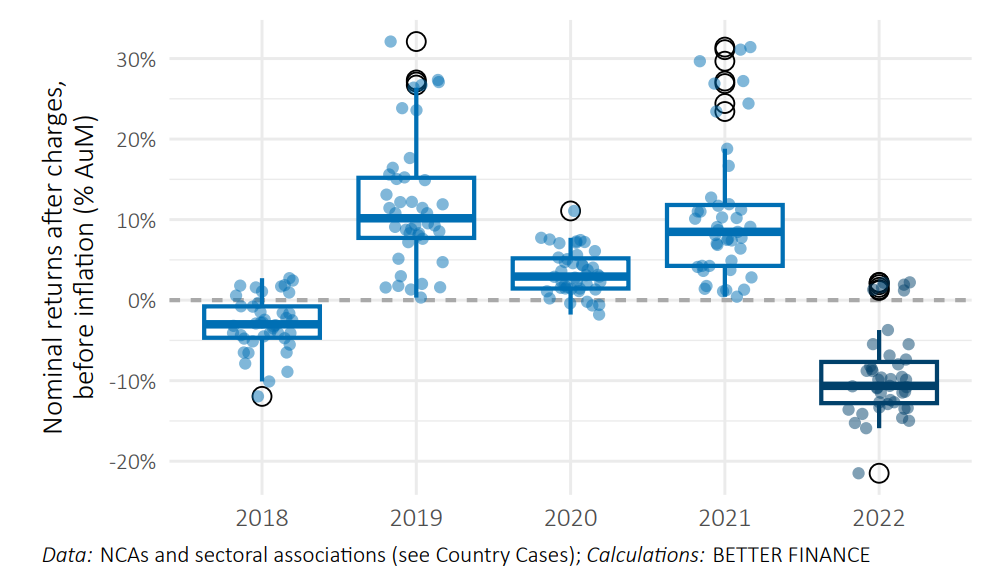

The report describes 2022 as an "annus horribilis" for European pension savers, who struggled with low returns across various product categories, worsened by high inflation rates that eroded their purchasing power. It examined long-term and pension savings in 17 EU Member States, revealing a significant decline in nominal returns that failed to keep pace with inflation.

Asset allocation woes

One of the main issues identified is asset allocation, with heavy investment in low-yield, high-fees bonds.

“Regulations governing long‐term and pension savings should not discriminate against long‐term equity investments,” the report reads. “Specifically, life‐cycling strategies that adjust risk to the investment horizon of the saver should enable managers to invest a substantial portion of younger investors’ contributions or premiums in equity market instruments.”

The lack of transparency in fees and charges further complicates savers' ability to compare pension providers and products effectively.

Better Finance's policy recommendations aim to tackle the challenges faced by EU pension savers. These include improving reporting standards, curbing conflicts of interest, advocating for better governance, and standardising investor information. They also emphasise the need for clearer information on the sustainability of EU long-term and pension savings.

The report proposes adjusting taxation to real values to avoid penalising long-term and pension products and suggests introducing auto-enrolment in occupational pensions to promote consistent retirement savings.

Average 1‐yr returns of pension funds in 17 EU countries: