Private investment-laden portfolios of US university funds achieved a net return of 7.7 per cent in FY2023, but the gains were almost entirely due to public equities.

Historically, university funds with larger endowments tend to achieve better one-year investment returns than funds with smaller endowments due to significant allocations to private investing. The rise in the US stock market and disappointing returns on alternative investments reversed the trend in 2023.

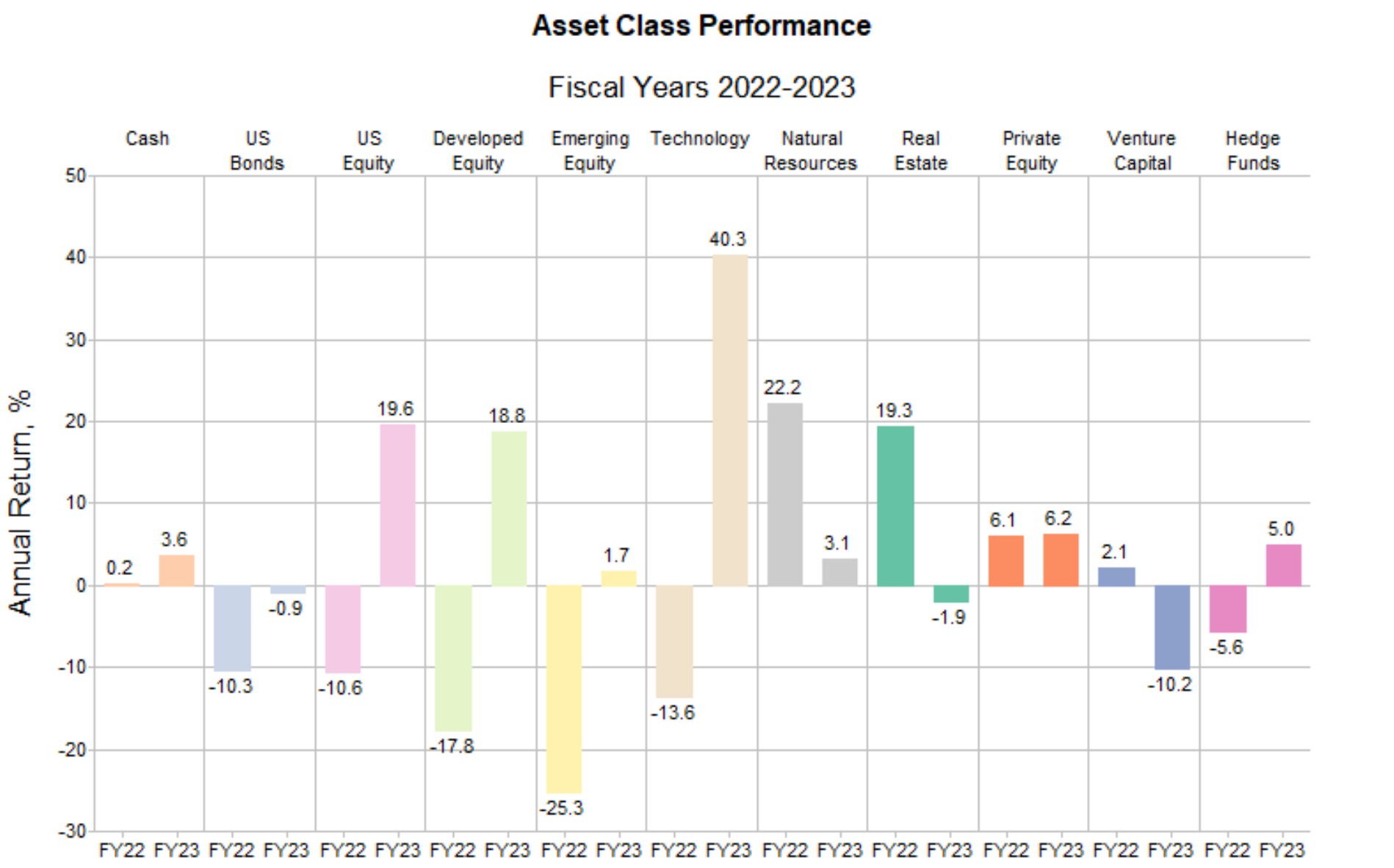

University funds, so-called "endowments", traditionally follow the "Yale model" in which less is allocated to traditional stocks and bonds than in a balanced fund, and more to alternative investments such as private equity, venture capital, hedge funds and real estate. Endowments on average have double-digit allocations to private equity (17.1 per cent); marketable alternatives (15.9 per cent) and venture capital (11.9 per cent).

Funds with assets greater than five billion dollars achieved an average return of 2.8 per cent during the financial year, while funds with less than 50 million dollars in assets achieved an average return of 9.8 per cent, reports the national advocacy organisation for US university endowments NaCuBo, which examined the data of 688 funds with combined assets under management of 840 billion dollars.

Ivy League

According to data from research firm MPI, Ivy-league university funds in particular performed outright poorly in fiscal 2023. They achieved an average return of 2.1 per cent, while a global 70/30 benchmark posted 11.1 per cent gains. The disappointing results are almost entirely attributable to investments in venture capital.

“As we predicted back in May 2023, venture capital allocations were the biggest drag on Ivy endowments, with private equity offering little compensation with low (albeit positive) returns. 2023 reminded us how difficult it can be to outsmart a low-cost, liquid balanced portfolio (70/30),” the MPI report said.

On private equity investments, funds earned 6.1 per cent on average, on venture capital investments, funds lost 10.2 per cent on average, according to MPI's Ivy Report Card subtitled “Volatility Laundering And The Hangover From Private Markets”.

Among non-alternative double-digit allocations of endowments in 2023 were US equities (12.5 per cent), real estate (11.2 per cent) and fixed income (11.0 per cent).

Domestic equities, especially mega-cap technology stocks epitomised by the Magnificent 7, are currently doing extremely well again, and although interest rates have risen recently, bonds have also performed positively year-to-date in fiscal terms.

“Schools with relatively traditional or vanilla portfolios with higher relative exposure to US public markets will outperform again in 2024 if current asset class performance persists,” said Michael Markov, CEO of MPI.

The end of the Yale model?

Although the long-term performance of private assets in university portfolios remains intact, Yale's chief investment officer Matt Mendelsohn has openly questioned the sustainability of his university's famous investment strategy.

“I spend most of my time thinking about how to adapt the Yale Model to a ‘more competitive and uncertain environment’,” he wrote in an open letter in October. “We are at an economic turning point, as the 40-year trend of falling interest rates reverses. However, one thing is certain: success in the next four decades will look different from success in the past four,” Mendelsohn said.

According to the cio, the university can and should maintain a significant allocation to illiquid investments, but “illiquidity by itself does not produce excessive returns,” Mendelsohn wrote. “We need to be careful when investing the fund with a view to ensuring the stability of critical support for the operating budget from year to year.”

Investment report card for the top US universities